Navigating the Mortgage Process in 2026: A Guide to Success

Navigating the Mortgage Process in 2026: A Guide to Success

Key Takeaways

- Maintaining financial stability is the most critical factor during the mortgage process.

- Avoid any major changes to your credit, income, or assets until your loan is officially closed.

- The 2026 market has seen adjustments to loan limits, reflecting a dynamic housing landscape.

- Partnering with a trusted loan advisor can help you navigate the complexities with confidence.

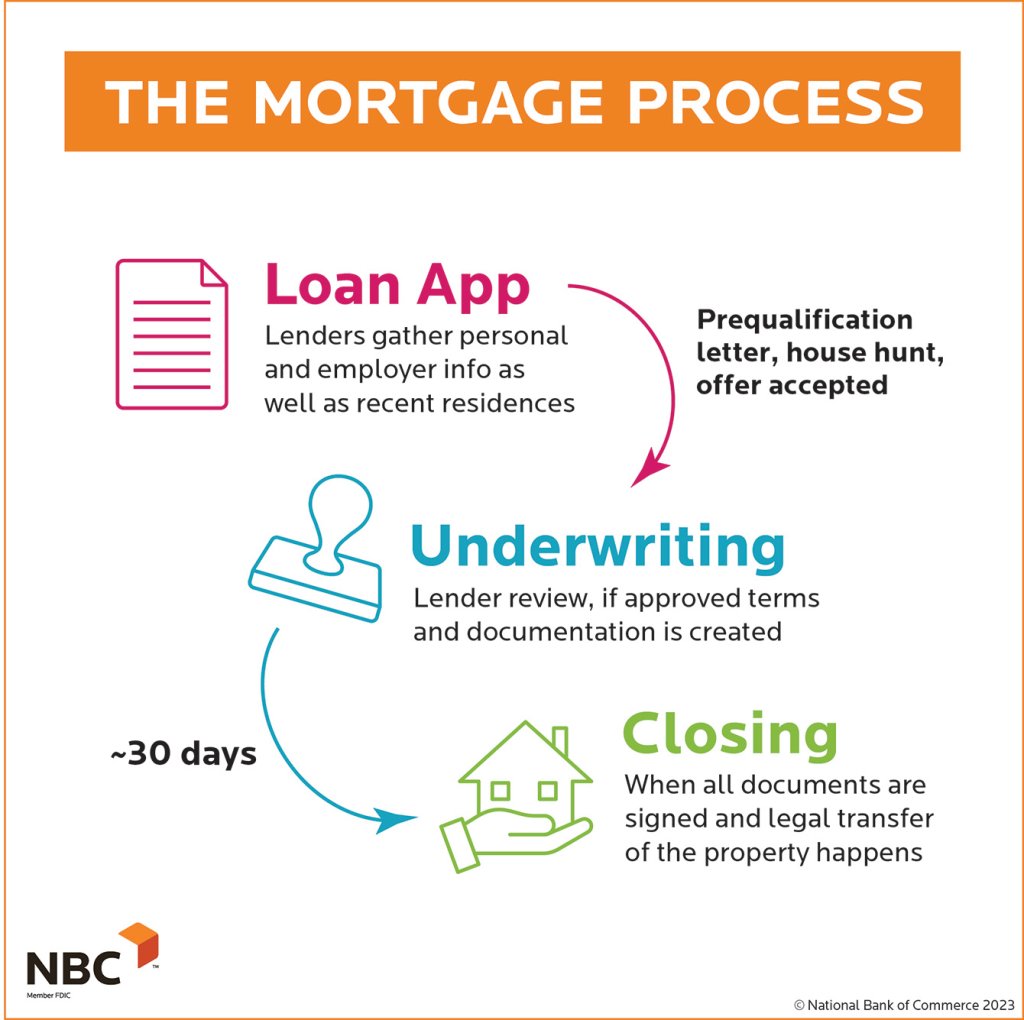

Securing a mortgage is one of the most significant financial steps you will take. While it can feel complex, understanding the key principles of the loan process can empower you to move forward smoothly and successfully. The journey doesn’t end at pre-approval; your financial habits are under review right up until you have the keys in hand.

This guide for 2026 will walk you through the essential do's and don'ts to ensure a seamless path to homeownership.

The Golden Rules: What You SHOULD Do

Think of the time between your loan application and closing as a quiet period for your finances. Your primary goal is to demonstrate consistency and reliability to your lender.

Maintain Stable Employment

Your income and employment history are the bedrock of your loan application. Lenders need to see a stable, predictable source of funds to be confident in your ability to repay the loan. It's best to avoid changing jobs or altering your compensation structure during this time.

Keep Your Credit Score Strong

Your credit score is a direct reflection of your financial responsibility. Continue to make all payments on time and in full, especially for credit cards, auto loans, and any other existing debts. A strong credit history is crucial for securing favorable loan terms.

Be Diligent with Documentation

Your loan team will request various financial documents, such as pay stubs, bank statements, and tax returns. Respond to these requests as quickly and thoroughly as possible. Organized, prompt communication can significantly speed up the underwriting process.

Common Pitfalls: What You Should NOT Do

Even small, well-intentioned financial moves can raise red flags for underwriters. Here are the most common mistakes to avoid while your loan is in process.

Don't Make Large Purchases

This is not the time to finance a new car, purchase furniture, or rack up credit card debt. Taking on new debt can increase your debt-to-income (DTI) ratio, a key metric lenders use to evaluate your application. A higher DTI can jeopardize your loan approval.

Don't Open or Close Credit Accounts

Opening new credit cards can negatively impact your credit score by lowering its average age. Similarly, closing old accounts can reduce your available credit, which may also have an adverse effect. It's best to leave your credit profile as-is.

Avoid Large, Undocumented Deposits

Any large cash deposits into your bank account will require a clear paper trail. Lenders must verify the source of all funds used for a down payment and closing costs. If you receive a gift from a family member, be sure to follow the proper gift fund documentation procedures with your loan officer.

Understanding the 2026 Loan Landscape

Loan limits are adjusted periodically to reflect changes in the housing market. For 2026, we have seen notable increases in federal loan limits, which can expand purchasing power for many buyers.

| Loan Type | 2025 Limit | 2026 Limit | Change |

|---|---|---|---|

| Conforming Loan | $806,500 | $832,750 | +$26,250 |

| FHA Loan Floor | $524,225 | $541,287 | +$17,062 |

| FHA Loan Ceiling | $1,249,125 | $1,249,125 | No Change |

Note: These national limits can vary by county, especially in high-cost areas. Current market rates for a 30-year fixed-rate mortgage are in the 6.0%-6.15% range as of early 2026.

A Look at the Spokane Market

For those looking to buy in the Spokane metro area, the market shows signs of a healthy rebalancing. The median home price is currently estimated between $380,000 and $425,000.

More encouragingly for buyers, housing inventory has increased by approximately 19% year-over-year, providing more options to choose from. This has been met with steady demand, as home sales saw a modest 2.5% increase in 2025.

Your Trusted Partner in Homeownership

The mortgage process requires careful attention to detail, but it doesn't have to be overwhelming. By following these guidelines and working closely with a knowledgeable team, you can navigate the path to closing with confidence.

If you have questions about your specific situation or are ready to begin your homebuying journey, the experienced team at Q Home Loans is here to help.

This content is for educational purposes only and does not constitute a loan commitment or guarantee. Loan approval is subject to credit and property approval. Contact Q Home Loans for current rates and program availability. Q Home Loans is a division of American Pacific Mortgage Corporation, NMLS #1850. Equal Housing Lender.

Share this article

About the Author

Q Home Loans Team is a mortgage loan officer at Q Home Loans, dedicated to helping families achieve their homeownership dreams.

Meet Our Team